Deceleration in EV Sales and the Potential Impact on the U.S. Automotive Industry

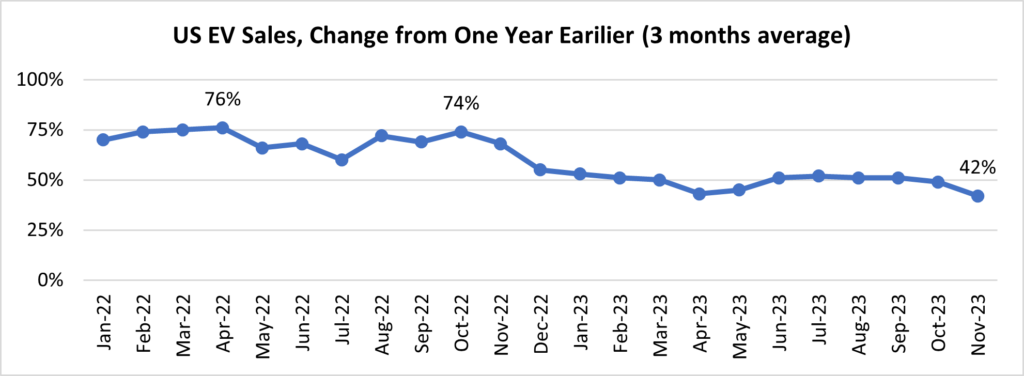

The United States has achieved a significant milestone in its quest for electrification, with over 1.2 million new Electric Vehicles (EVs) sold in the past year, representing more than 7.5% of total U.S. light vehicle sales in 2023, up from 5.9% in 2022 (Kelley Blue Book). However, this growth pales in comparison to the over 50% year-over-year surge experienced by the EV industry before 2023.

In the earlier years, EVs witnessed remarkable sales growth, even with models averaging over $65,000, fueled by high demand, low inventories, and optimistic sales projections by automakers. The appeal of EVs was heightened as gasoline prices approached $5 per gallon. Fast forward to the present, with gasoline prices now around $3 per gallon nationwide, and the average transaction price for an EV, without incentives, dropping to just under $52,000. This shift has seen the market transition from tech-savvy early adopters to more price-sensitive buyers.

(Source: WSJ, Motor Intelligence)

The most appalling change came from California, the leading state for EV penetration. The registration of electric light vehicles in California declined from the second quarter to the fourth quarter of 2023. About 103k EVs were registered in Q2, then went to 101,151 in Q3 and decreased to 89,993 in Q4. (Sources: Experian Automotive, Automotive News)

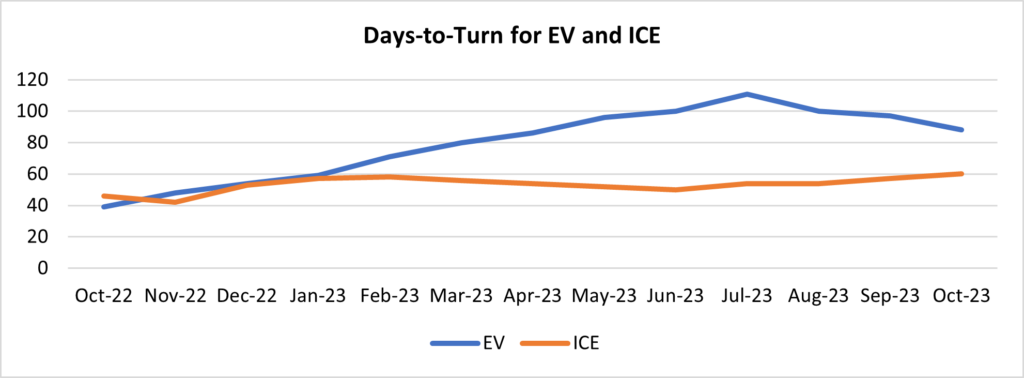

Over the past year, the EV market has faced challenges with price reductions and increasing inventories. In late 2023, it took almost twice as long to sell an EV in the U.S. compared to the previous year. The days-to-turn metric (how long it takes for a vehicle to sell once it is at a dealership) for EVs reached 57 days, compared to 39 days a year before, signaling a lengthening sales cycle. In contrast, ICEs took only 10 more days to turn compared to late 2022.

(Source: Cox Automotive, Edmunds)

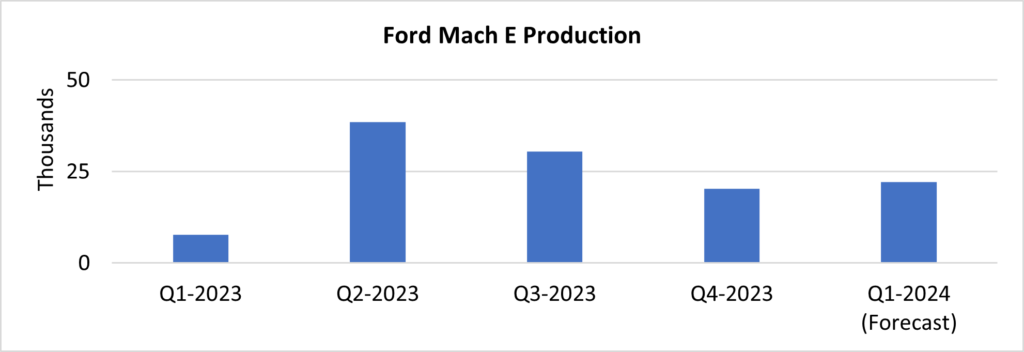

As the growth of EV sales came to a standstill in the latter part of 2023, leading to a buildup of EV inventory, several automakers opted to scale back their ambitious plans for EV rollouts, especially in the short term. Ford recently made announcements about postponing the construction of a new EV battery plant, downsizing another facility, and deferring $12 billion in planned electric vehicle expenditures. Additionally, Ford has scaled down production of the Mustang Mach-E since the fourth quarter of 2023. General Motors followed suit by delaying the launch of Chevrolet Silverado EV and GMC Sierra EV production in suburban Detroit, pushing it to late 2025. Furthermore, GM abandoned a collaboration with Japan’s Honda for the production of affordable EVs and postponed the retooling of an EV plant.

The price war initiated by Tesla indicates that sales are slowing down for all EVs. Furthermore, the price decrease triggers uncertainty with new customers on the sustainability of the market, and It rises anger with existing ones who instantly see the residual value of their vehicle dropping.

(Source: GlobalData Forecast Dec-2023)

The cautious perspective on the future of EVs is influencing decisions regarding investment allocation and the prioritization of product programs. Suppliers are now diverting attention to sustaining sales in their internal combustion components business while awaiting the growth of their EV ventures.

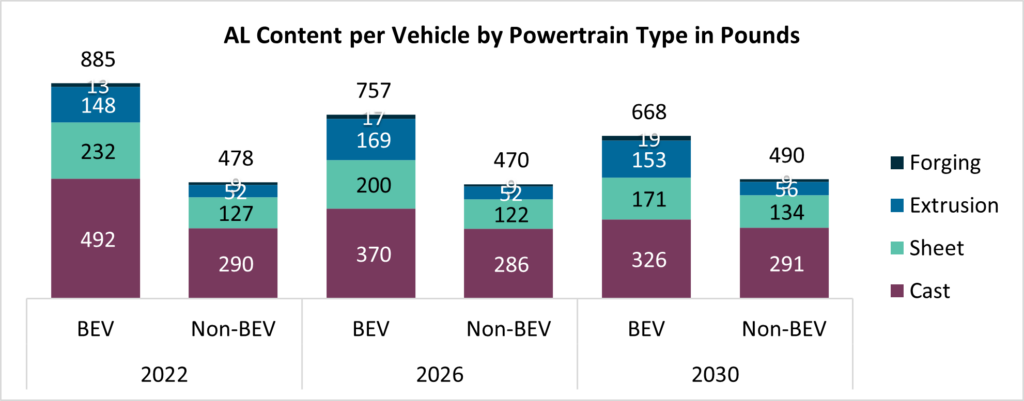

The sluggish adoption of electric vehicles is prompting manufacturers and suppliers to reassess their electrification strategies, given the disparities in material and component choices between EVs and Internal Combustion Engine (ICE) vehicles. An illustrative example is the utilization of aluminum. As highlighted in a 2023 aluminum study by Ducker Carlisle, Battery Electric Vehicles (BEVs) generally incorporate more aluminum content, driven by the increased demand for lightweight components. Suppliers are strategically expanding their capacity for aluminum parts, including battery packs, e-drives, body-in-white, chassis, closures, and other crucial components.

(Source: Ducker Carlisle)

While certain components can seamlessly transition between internal combustion, hybrid, and battery-electric vehicles, others may not be applicable to both EV and internal combustion platforms or may necessitate significantly different designs, leading to substantial investments by suppliers. This slowdown may also lead to increased resource and platform sharing among manufacturers, adaptation of existing assembly lines for EVs, standardization of parts, a focus on production costs, and redesigning cost-sharing mechanisms for future EV models. These measures are expected to result in fewer launches and a reduction in tooling expenditure.

Interestingly, not everyone views the slowdown in EV sales negatively. Auto companies’ EV transition strategies are also influenced by geopolitical factors and the federal government’s initiative to re-shore auto production in the U.S. for EVs. Finished EVs, batteries, e-drives, and other critical components manufactured or assembled by foreign entities of concern, such as China or Russia, will no longer qualify for the EV tax credit. This restriction has compelled OEMs and suppliers to redesign their footprint and supply chain, a process that could take years to complete. Some critical raw materials essential for e-drives and EV batteries, such as automotive-grade electrical steel and rare earth minerals, remain challenging to source domestically or from U.S. allied countries.

Amidst these changes, the EV industry sees a silver lining in the temporary slowdown, providing an opportunity to build a secure supply chain that exclude China sourced materials or components. The pause allows for breathing room in investment, permitting, and construction of a robust battery and e-drive supply chain, fostering domestic manufacturing and securing raw materials from reliable sources.

The deceleration in EV sales has prompted adjustments in plans and strategies across the automotive industry, leading to a reevaluation of priorities, reassessing the tipping point for new components, and a shift towards building a more sustainable and secure future for electric vehicles in the United States.

Ducker Carlisle’s decades of automotive consulting experience and comprehensive expertise in auto and light truck manufacturing, electrification, aftersales, and parts benchmarking help automotive clients secure an advantage in a shifting global market. Learn more here.

Article Prepared By:

Bertrand Rakoto, Director – Global Automotive Practice Leader

Leonard Ling, Senior Analyst – Automotive Knowledge Manager